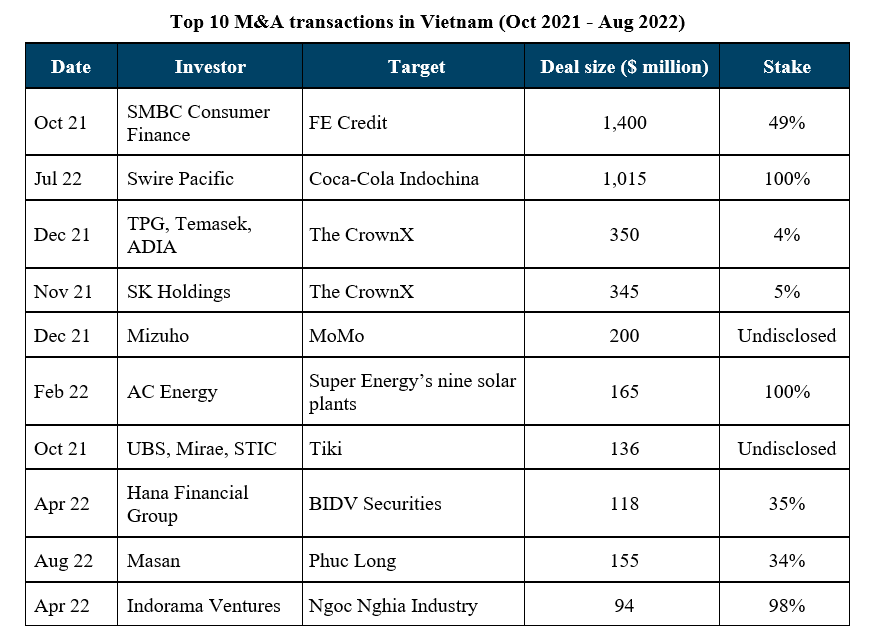

With the gradual unwinding of Covid-related restrictions and the resumption of international flights, M&A activity in Vietnam has accelerated and the outlook for deal-making is positive.

Photo: Viet Tuan

Vietnam’s economic recovery has proven appealing to investors, with it being one of only a few countries to record two consecutive years of GDP growth, in 2020 and 2021, during the height of Covid-19.

The General Statistics Office (GSO) put GDP growth in 2021 at 2.58 per cent, despite the country experiencing one of the strictest lockdowns in the world during the second half of the year. Looking ahead, the Asian Development Bank has forecast Vietnam’s economic growth to recover to 6.5 per cent this year. Growth in the second quarter actually came in at 7.7 per cent; the highest quarterly figure for a decade.

Pent-up deal-making demand is a key driver. Both strategic investors and financial sponsors have a large amount of capital to invest and are keen to identify new opportunities or revive discussions that were put on hold. Industry leaders are actively seeking acquisitions to consolidate market share within their verticals, taking advantage perhaps of competitors weakened by Covid and slower to rebound. In addition, many companies are looking to position themselves for recovery in the post-pandemic economy and need new capital injections for internal transformation and further growth in order to remain competitive.

The resumption of international travel is also significant. In-person due diligence and site visits have facilitated many deals that were previously put on hold, especially for asset-heavy industries such as industrials, logistics, and healthcare. Since last October, BDA has met with numerous foreign investors who have expressed a strong interest in Vietnam. After a two-year hiatus, BDA organized its annual networking event in Ho Chi Minh City in May, with over 200 participants - mainly investors and corporate shareholders - and all appreciated the opportunity to reconnect in person and discuss the future.

Trends to persist

Domestic investors had an advantage over their foreign counterparts during Covid given their local presence, and this led to an increase in domestic deal flow and volume. Although Covid-related border restrictions have now been lifted, BDA has seen local conglomerates continuing their acquisition spree in a market that has historically been dominated by foreign buyers.

For example, in addition to its investment in Phuc Long, Masan also acquired a 25 per cent stake in Trusting Social, a company engaged with credit scoring based on social data, for $65 million in April. This was another transaction in which BDA acted as the exclusive advisor to the target company. Nova Group has been on an acquisition spree, expanding its ecosystem with a focus on Consumer businesses, having acquired and taken over the operations of major F&B establishments such as Jumbo Seafood, Sushi Tei, Crystal Jade, and PhinDeli.

From a deal negotiation perspective, BDA has observed several points that have become particularly important during deal negotiations. With material adverse change (MAC) clauses, buyers and sellers now need to acknowledge the risk of a significant downturn in the business as a result of Covid-19. MAC provisions typically exclude market-wide macro-economic impact, but since Covid has different effects on different industries, the negotiation of specific triggers in MAC clauses needs to be scrutinized.

Earn-outs have become more common by bridging valuation gaps under scenarios of temporary uncertainty, while also enabling sellers to share in the upside of long-term growth. Warranty and indemnity (W&I) insurance, a rare option in Vietnam deals in the past, is also being used more frequently, as both buyers and sellers appreciate the benefit of a smoother and faster signing and closing process.

During the height of domestic lockdown and border restrictions in 2021, virtual interaction was the only option in most cases for merger and acquisition (M&A) transactions in Vietnam. We expect that for non-key discussions, virtual meetings will continue to be a common option in the future. However, for other key parts of the transaction process, such as site visits and due diligence, which were supported by on-the-ground advisors and virtual tours during Covid, and especially for negotiations, in-person participation will still be preferred going forward.

“There are a lot of high-quality assets in Vietnam that have proven resilient against Covid that are now well-positioned for robust growth. BDA Partners looks forward to a busy period ahead with a long list of current live deals and ongoing opportunities,” said Ms. Trinh Thu Huong, Partner, BDA Partners.

Source: Mergermarket

Global slowdown in M&As

Global M&As in the first half of 2022 were down 21 per cent in value and 17 per cent in volume compared to the first half of 2021, partly due to the cooldown in special purpose acquisition company (SPAC)-related transactions. Inflationary pressure across supply chains, geopolitical tensions, and a rising interest rate environment have also contributed to the volatility that could become a recurring theme in the M&A market over the next year or so.

Inasmuch as businesses in Vietnam are not immune from these factors, we still believe that 2022 will remain another busy year for Vietnam’s M&A market. Investors have not shown any reduced appetite in deal-making in the country, as evidenced by their interest in BDA’s ongoing mandates. We believe that there are a lot of high-quality assets that have proven resilient against turbulence brought about by Covid that are now well-positioned for robust growth, and we look forward to a busy period ahead with a long list of current live deals and ongoing opportunities.

Tailwinds for future growth in M&As in Vietnam include:

- Strong socio-economic backbone: Vietnam will still benefit from steady economic growth, political stability, and a bourgeoning middle class. Participation in multiple free trade agreements and open-market policies make it an attractive destination for foreign investment.

- Rising importance as a manufacturing hub: More global corporations are expected to relocate to Vietnam, as the country has made significant progress in infrastructure development to catch up with international standards, with major investments from both public and private sectors. The US-China trade war and prolonged Covid restrictions in China have also led to more manufacturers moving operations to Vietnam.

- Improving regulatory landscape: It is worth noting that with regards to M&A regulation and processes, local authorities have continually been improving their turn-around times while working towards clearer guidelines. For example, Decree No. 155/ND-CP guiding the implementation of the Law on Securities, which took effect in 2021, has provided additional clarification and detailed guidance with regard to the public tender offer process and foreign ownership limits.

- Growing familiarity with M&As: Local businesses are becoming more professional, with strong management teams and better corporate governance. Vietnamese companies are now more familiar with M&A concepts and are open to considering strategic partnerships with foreign investors, who can provide support through best practices in business operations and have extensive experience from global markets.

Most attractive sectors

Consumer: The Consumer sector will continue to be one of the main drivers of transaction volume. Investors will target Vietnam as one of the fastest-growing economies in the region, with its growing middle class and young population with increasing incomes and a propensity to spend.

Healthcare: In response to the lack of capacity within the national healthcare system, there has been an ongoing shift in demand towards private care. Private hospitals will continue to attract interest from both strategic and financial investors, especially as patient volumes and occupancy rates are recovering to pre-Covid levels, while more profitable surgeries and procedures are re-introduced.

Education: Within private education, both local and international schools had received significant interest from investors before Covid appeared. We expect discussions regarding education assets to be restarted in the near future, as business performance recovers now that students of all levels have returned to classrooms.

Logistics: Tailwinds from high growth in exports, a booming internet economy, and supply chain shifts from China will continue to propel growth in Vietnam’s logistics industry. Assets in warehousing (especially smart logistics) and cold chains will generate strong interest from global investors.

Financial Services: An underbanked population with a shortage of financing and credit solutions will spur further investments in financial services. The focus will be on consumer finance / fintech companies that provide solutions to enable access to non-bank credit for both individuals and micro, small, and medium-sized enterprises.

Renewable Energy: With a rapidly-growing economy, Vietnam has been at risk of power shortages due to a lack of power infrastructure. Capital injections into the development of renewable energy could provide a suitable solution. Attractive feed-in-tariffs and untapped potential in solar and wind power capacity will make Vietnam an attractive destination for investors.

Sáu giải pháp phát triển nhanh và bền vững ngành năng lượng

Việt Nam đang đứng trước cơ hội lớn để phát triển năng lượng xanh, sạch nhằm đảm bảo an ninh năng lượng và phát triển bền vững. Ông Nguyễn Ngọc Trung chia sẻ với Tạp chí Kinh tế Việt Nam/VnEconomy về sáu giải pháp để phát triển nhanh và bền vững ngành năng lượng nói chung và các nguồn năng lượng tái tạo, năng lượng mới nói riêng…

Nhân lực là “chìa khóa” phát triển điện hạt nhân thành công và hiệu quả

Trao đổi với Tạp chí Kinh tế Việt Nam/VnEconomy, TS. Trần Chí Thành, Viện trưởng Viện Năng lượng nguyên tử Việt Nam, nhấn mạnh vấn đề quan trọng nhất khi phát triển điện hạt nhân ở Việt Nam là nguồn nhân lực, xây dựng năng lực, đào tạo nhân lực giỏi để tham gia vào triển khai, vận hành dự án...

Phát triển năng lượng tái tạo, xanh, sạch: Nền tảng cho tăng trưởng kinh tế trong dài hạn

Quốc hội đã chốt chỉ tiêu tăng trưởng kinh tế 8% cho năm 2025 và tăng trưởng hai chữ số cho giai đoạn 2026 – 2030. Để đạt được mục tiêu này, một trong những nguồn lực có tính nền tảng và huyết mạch chính là điện năng và các nguồn năng lượng xanh, sạch…

Nhà đầu tư điện gió ngoài khơi tại Việt Nam vẫn đang ‘mò mẫm trong bóng tối’

Trả lời VnEconomy bên lề Diễn đàn năng lượng xanh Việt Nam 2025, đại diện doanh nghiệp đầu tư năng lượng tái tạo nhận định rằng Chính phủ cần nhanh chóng ban hành các thủ tục và quy trình pháp lý nếu muốn nhà đầu tư nước ngoài rót vốn vào các dự án điện gió ngoài khơi của Việt Nam...

Tìm lộ trình hợp lý nhất cho năng lượng xanh tại Việt Nam

Chiều 31/3, tại Hà Nội, Hội Khoa học Kinh tế Việt Nam, Hiệp hội Năng lượng sạch Việt Nam chủ trì, phối hợp với Tạp chí Kinh tế Việt Nam tổ chức Diễn đàn Năng lượng Việt Nam 2025 với chủ đề: “Năng lượng xanh, sạch kiến tạo kỷ nguyên kinh tế mới - Giải pháp thúc đẩy phát triển nhanh các nguồn năng lượng mới”...

Thuế đối ứng của Mỹ có ảnh hướng thế nào đến chứng khoán?

Chính sách thuế quan mới của Mỹ, đặc biệt với mức thuế đối ứng 20% áp dụng từ ngày 7/8/2025 (giảm từ 46% sau đàm phán),

có tác động đáng kể đến kinh tế Việt Nam do sự phụ thuộc lớn vào xuất khẩu sang Mỹ (chiếm ~30% kim ngạch xuất khẩu).

Dưới đây là phân tích ngắn gọn về các ảnh hưởng chính:

![[Interactive]: Toàn cảnh kinh tế Việt Nam tháng 7/2025](https://media.vneconomy.vn/302x182/images/upload/2025/08/0675413e3e-4a53-4c15-ae1f-e8883264607e.png)

![[Phóng sự ảnh] Những điểm nhấn đặc biệt sẽ xuất hiện tại đại nhạc hội “Tổ quốc trong tim”](https://premedia.vneconomy.vn/files/uploads/2025/08/10/51be9bdd24cf4dfc86a030e2b6e3db11-2906.jpg?w=302&h=182&mode=crop)